The current macroeconomic environment, characterised by rising prices and tighter financial conditions, is likely to weigh on companies’ ability to service their debt. We measure a company’s debt-servicing ability through their interest coverage ratio (ICR), which is the amount of times a company’s earnings can cover the interest paid on their debt.

Companies with low ICRs are more likely to experience payment difficulties, which could lead to default or reductions in investment and employment. Many companies doing either of these at the same time could pose a risk to financial stability and economic growth.

Both company earnings and interest payments are affected by global economic developments. The rapid rise in input costs could compress companies’ profit margins, while a rise in Bank Rate typically pushes up interest costs.

We estimate large-company ICRs which would be consistent with the central projection in the August Monetary Policy Report by projecting the earnings and interest paid channels under the assumption that corporate indebtedness remains unchanged:

- Earnings: we use ONS input-output tables (which measure the inputs industries use to produce their products) to understand how the increase in energy and fuel prices affects prices across industries. Making some assumptions, eg no changes in demand, we can estimate the impact on a company’s earnings as a result of the rise in energy and fuel prices.

- Interest paid: we model the increase in companies’ interest payments based on market expectations for an increase in Bank Rate to around 2.75% by the end of 2022 as well as a rise in funding spreads. We do not know what portion of each individual company’s debt is likely to reprice during 2022, so we run a series of experiments assuming varying shares of fixed and floating debt per company, in line with aggregate statistics. The median of these experiments represents our central case for the impact of higher interest rates.

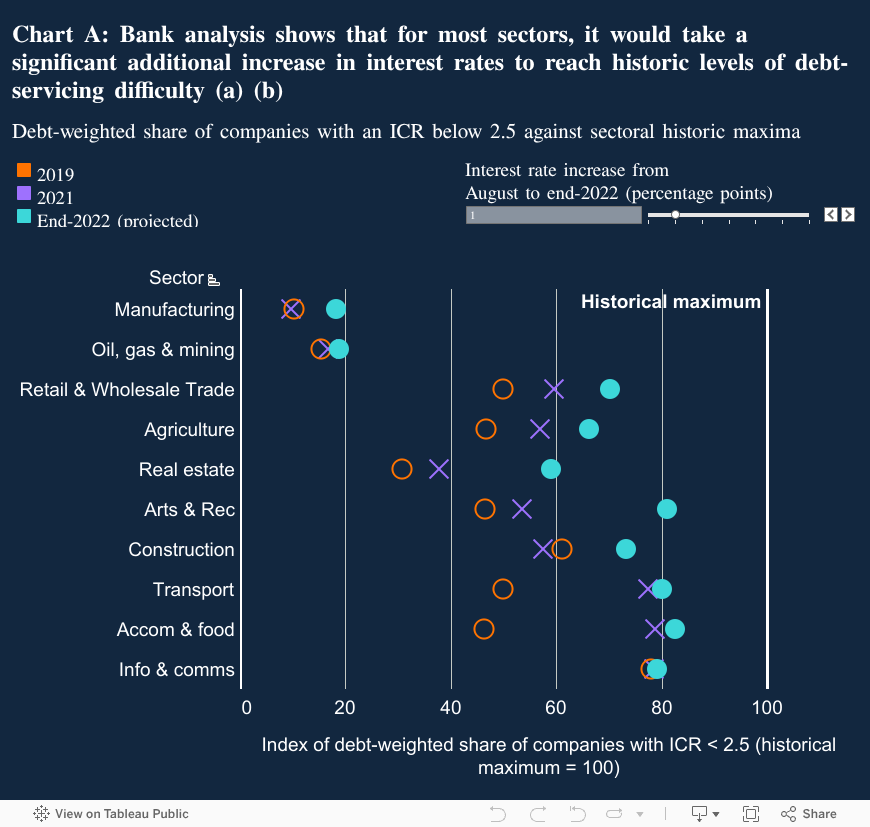

The results of this exercise can be seen in Chart A. The combined interest rate and earnings shock increases the share of companies with an ICR below 2.5 (a threshold below which companies are more likely to experience repayment difficulties) across sectors from 36% in 2021 to 45% in 2022. This is a significant rise, though well under the historical high of 62%, attained in 2001. We estimate that funding costs would need to rise by around 500 basis points over the market implied Bank Rate path for 2022 to approach this historic peak.

This projected deterioration in debt serviceability is driven by the rise in interest rates, with lower company earnings having a smaller impact. This is intuitive, as we use the conservative assumption that nominal business earnings remain broadly flat in aggregate in 2022. Within industries, it is likely that individual companies’ ICRs would be more sensitive to earnings reflecting company-specific variation in energy costs and product demand that we do not model here.

Overall, the Financial Policy Committee (FPC) assesses that UK corporate debt vulnerabilities are likely to increase in the near term, with many businesses likely to face cost challenges, but major UK banks are resilient to these vulnerabilities.

Footnotes

- Sources: Bureau van Dijk, ONS, S&P Capital IQ and Bank calculations.

- (a) Interest rate increases refer to any change since 12 August 2022. The starting selection of +1 percentage point is consistent with market-implied expectations for Bank Rate to rise to around 2.75% by end-2022.

- (b) The sample consists of UK-owned firms with a turnover greater than £10.2 million.

This post was prepared with the help of Jelle Barkema & Lindsey Rice-Jones.

This analysis was previously published in the Financial Policy Report in July 2022.

Share your thoughts with us at BankOverground@bankofengland.co.uk