How do we know what the rate of inflation is?

Every month, the Office for National Statistics checks the prices of about 700 items in a ‘basket’ of goods and services, which is designed to represent what people buy on average.

The basket includes everyday items (eg a loaf of bread and a bus ticket) but also includes much larger ones, such as a car and a holiday. The basket’s overall price is known as the Consumer Price Index.

To calculate the rate of inflation, they compare the CPI with what it was a year ago. The change in the price level over the year is the rate of inflation.

For example, if CPI inflation is 2%, then a basket that was £100 a year ago would be £102 today.

You can use our inflation calculator to see how prices have changed over time.

Current inflation rate 3.2%

Target: 2%

What does % mean?

% is the sign for ‘per cent’, which means ‘out of 100’.

If something costs £10 and it goes up by 2%, then it would cost £10.20p. That is an increase of 20p.

If the amount you start with is bigger, then the size of the increase will be greater – even though the percentage change is the same.

So, if something with a price tag of £1,000 goes up 2%, it would cost £20 more.

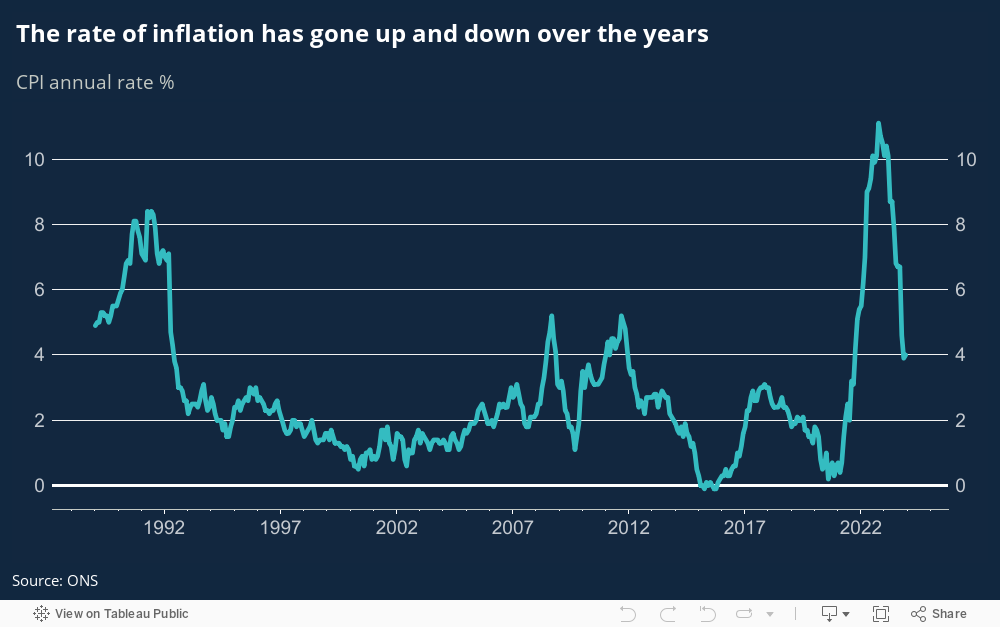

How has the rate of inflation changed over the years?

It has gone up and down. For most of the last 20 years, it has been about 2%. But it has been higher than that at times. And sometimes it has been lower.

Why is the rate of inflation important?

A low and stable rate of inflation helps to create a healthy economy.

The Government sets a target for how much overall prices should go up each year in the UK. That target is 2% and it is the Bank of England’s job to keep inflation at that rate.

The 2% target is similar to that of many other countries. It is low enough to keep price rises small but high enough to avoid the problem of deflation – which is when overall prices fall, and businesses make less money and begin to cut costs by reducing wages and staff. This can lead to lower incomes and increased unemployment.

So, a little bit of inflation is helpful. But high and unstable rates of inflation can be harmful.

If prices are unpredictable, it is difficult for you to plan how much you can spend, save or invest.

In extreme cases, high and volatile inflation can cause an economy to collapse. This happened in Zimbabwe in 2007-2009 when price levels increased by about 80 billion per cent in a month. As a result, people simply refused to use Zimbabwean banknotes and the economy ground to a halt.

What does the Bank of England do to keep inflation low and stable?

The main way is through interest rates.

An interest rate tells you how high the cost of borrowing is, or how high the rewards are for saving.

If you are a borrower, the interest rate (or lending rate) is the amount you are charged for borrowing money – shown as a percentage of the total amount of the loan. The higher the percentage, the more you must pay back.

If you are a saver, the interest rate (or savings rate) tells you how much money will be paid into your account, as a percentage of your savings. The higher the savings rate, the more you will get.

So, what is the link between the interest rates and inflation?

Higher interest rates make it more expensive for people to borrow money and encourage them to save. This means that, overall, they will tend to spend less.

If people spend less on goods and services, prices will tend to rise more slowly. That lowers the rate of inflation.

The reverse is also true.

Lower interest rates mean it is cheaper to borrow money and there is less of an incentive to save. This encourages people to spend and increases the rate of inflation.

How does the Bank influence interest rates?

Two main ways:

- We set Bank Rate, also known as the base rate. This is the most important interest rate in the UK because it influences all other interest rates.

- We can buy and sell bonds from financial markets to support spending in the economy. We mainly buy government bonds, or ‘gilts’. Buying assets in this way is called quantitative easing (QE). QE allows us to influence the interest rates on savings and loans. We used it when interest rates were very low (almost at zero).

What links the cost of living and inflation?

The prices you pay at the supermarket, the petrol pump and many other places have risen quickly in recent years. Inflation is the measure of the speed of those increases.

When prices are rising quickly, it means inflation is high and you can’t buy as much with your money. Therefore, the cost of living is higher.

The Government sets us a target of ensuring inflation is low and stable at 2%. As the UK’s central bank, the best tool we have to slow down the rate of rising prices is interest rates.

Between 1997 and 2021, CPI inflation was 2% on average – in line with our target. It began to rise in 2021 and reached a peak of 11% in 2022. It has fallen back to about 2% since then.