The sterling money markets play a key role in the implementation and transmission of monetary policy. The Bank now collects granular data on sterling money market transactions, providing new insights into these markets. A subset of these Sterling Money Market (SMM) data will, from April, be used as the inputs to the sterling overnight index average (SONIA) benchmark, as planned reforms take effect.

To increase market transparency, the Bank intends to use the new data to publish summary statistics of activity in the broader sterling money markets on a regular basis. This article presents example statistics for the first time.

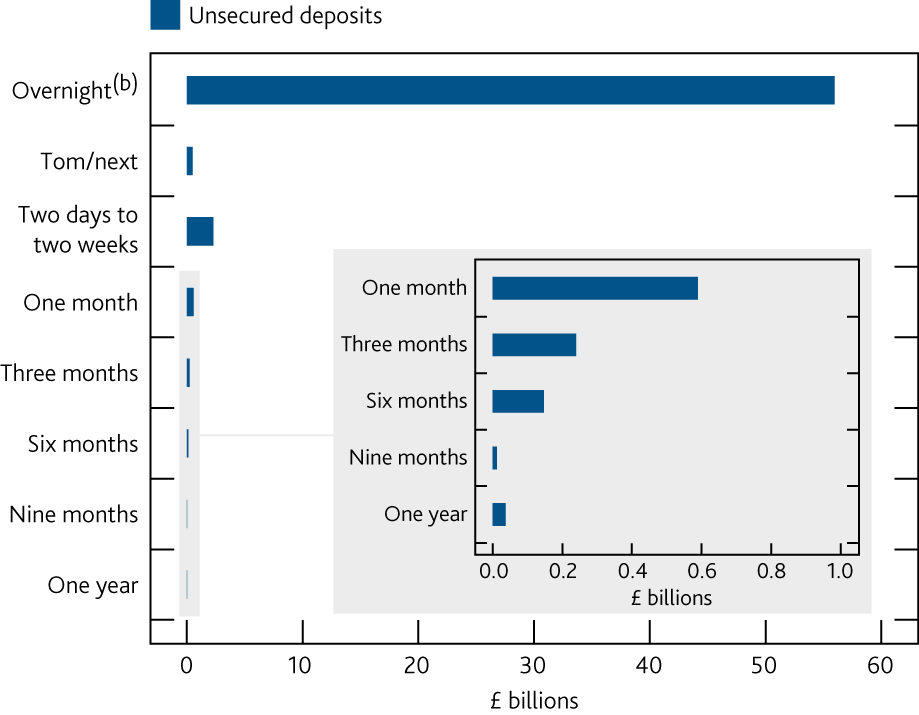

We also use this new, comprehensive data set to shed light on the market for term unsecured deposits. Transactions are overwhelmingly completed overnight. Beyond that maturity, the average daily value of term deposit transactions is generally low (summary chart), rarely exceeding £1 billion at maturities of one month or longer. Average rates at these terms are also highly volatile, albeit around a clear trend.

By comparison, the average value of transactions soon to underpin SONIA - capturing overnight unsecured deposits which are £25 million or larger - has been on average close to £50 billion per day, and the headline rate is very stable.

Underlying this stability, our analysis suggests that there is an active core of depositors in the overnight unsecured market measured by SONIA. We find evidence of a dynamic pattern of bank-depositor relationships, consistent with a competitive market environment where depositors can, and do, move their business around.