By Frank Kenny of the Bank’s Foreign Exchange Division and David Mallaburn of the Bank’s Capital Markets Division.

Hedge funds are of interest to the Bank because of: their importance for secondary market liquidity and price discovery; the significant use of leverage by some types of hedge funds; and their interconnections with a range of counterparties. Risks from and to hedge funds are therefore relevant to the Bank’s Financial Policy Committee, whose primary objective is to identify, assess, monitor and take action in relation to financial stability risks across the UK financial system.

The global hedge fund industry has experienced dramatic growth since 2000, with assets under management increasing from US$250 billion to over US$3.5 trillion in 2017. Hedge funds operate a number of different strategies which dictate the markets they invest in and the leverage that they take.

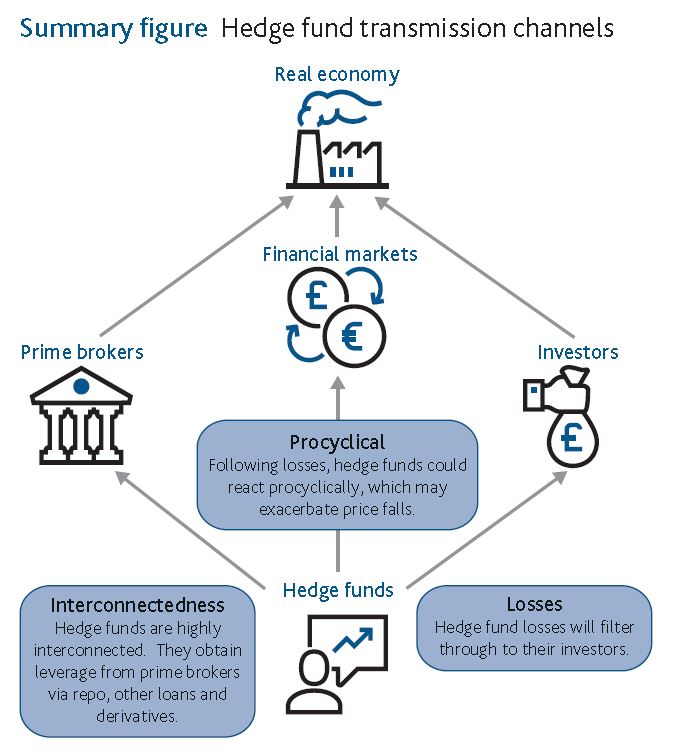

Hedge funds are exposed to a number of risks, including risks from using leverage and liquidity risks from investor redemptions. Hedge funds can also transmit risk to the financial system (summary figure). Since the financial crisis, there have been changes which may serve to mitigate some of the risks. Hedge funds themselves have adjusted their business models, and international regulations, such as the Financial Stability Board’s derivative reforms, have limited the risks that hedge funds pose to the financial system.