Key findings

- The outstanding value of all residential mortgage loans increased by 0.8% from the previous quarter to £1,734.4 billion, the highest stock of outstanding mortgage loans since reporting began in 2007, and was 3.0% higher than a year earlier (Table A).1

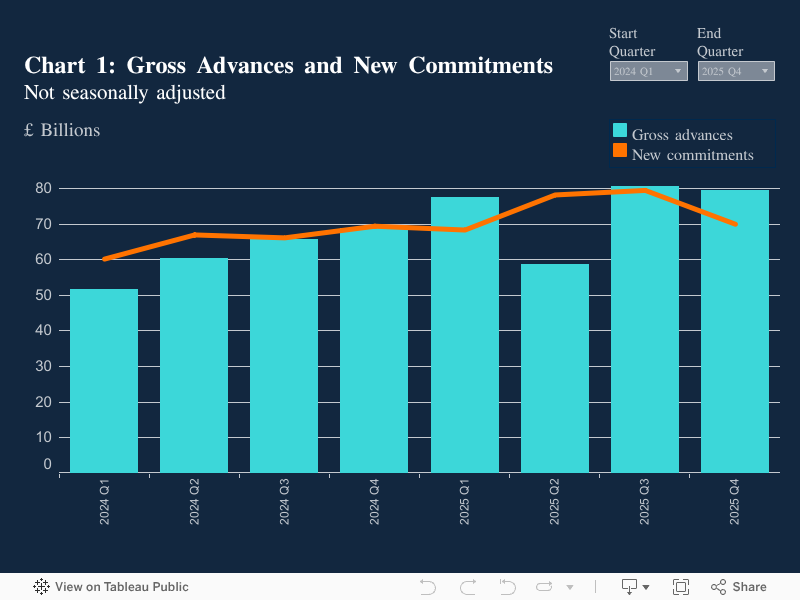

- The value of gross mortgage advances decreased by 1.3% from the previous quarter to £79.4 billion, but remained 15.4% higher than a year earlier (Table A and Chart 1).

- The value of new mortgage commitments decreased by 11.9% from the previous quarter to £69.9 billion, the largest decrease since 2023 Q3, but remained 0.8% higher than a year earlier (Table A and Chart 1).

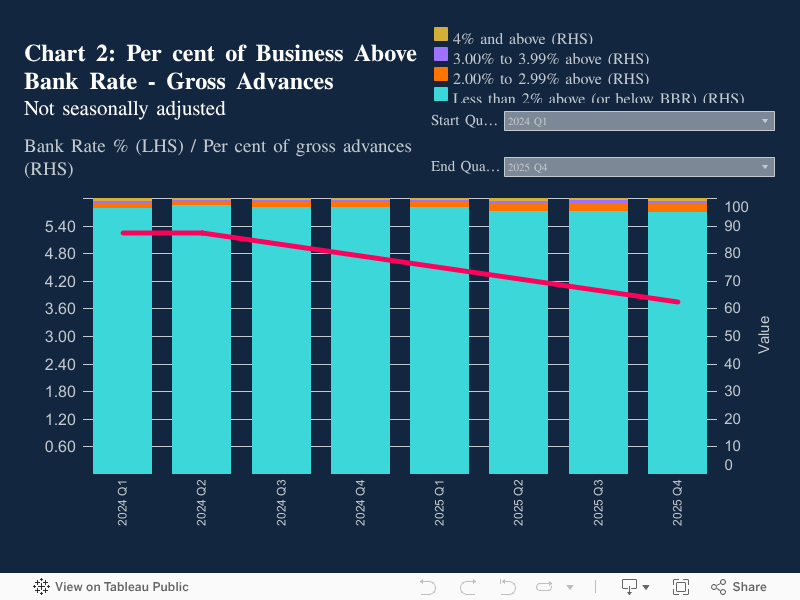

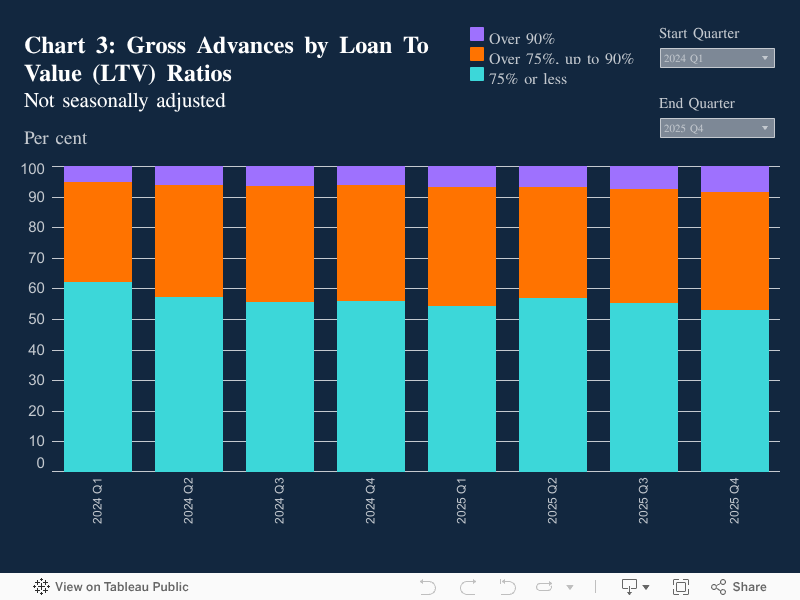

- The share of gross mortgage advances with loan-to-value (LTV) ratios exceeding 90% increased by 0.9pp from the previous quarter to 8.3%, the highest share since 2008 Q2, and was 2.1pp higher than a year earlier (Chart 3).

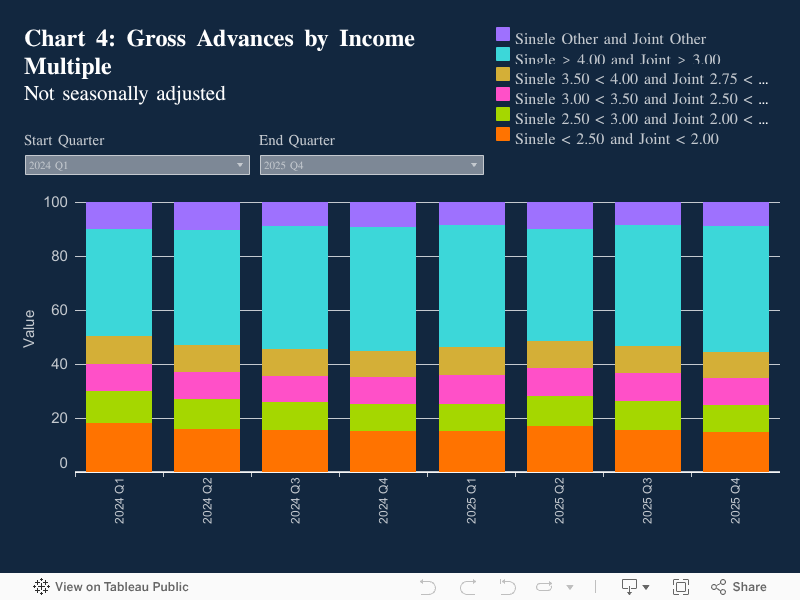

- The proportion of lending to borrowers with a high loan-to-income (LTI) ratio increased by 1.7 percentage points (pp) from the previous quarter to 46.5%, the highest since 2022 Q4, and was 0.6pp higher than a year earlier (Chart 4).

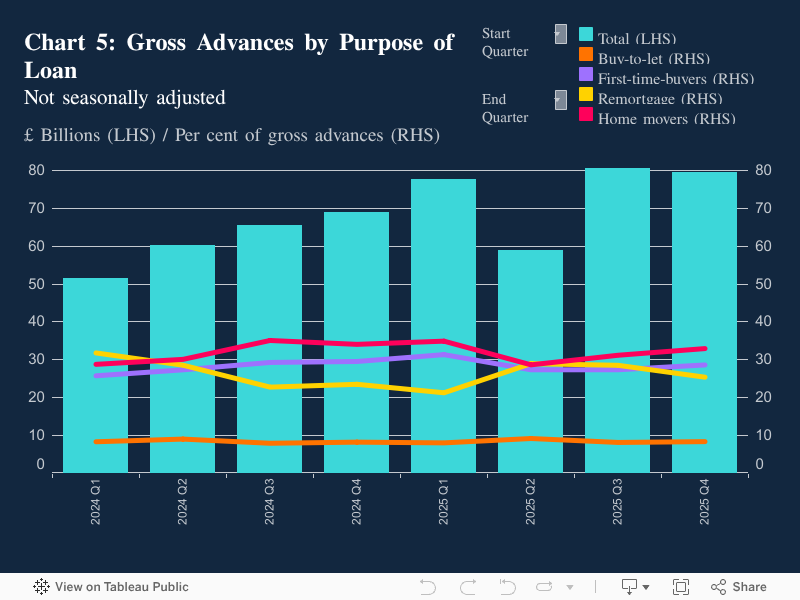

- The share of gross mortgage advances for buy-to-let purposes increased by 0.2pp from the previous quarter to 8.4%, and was 0.1pp higher than a year earlier (Chart 5).

- The share of gross mortgage advances for house purchase for owner occupation increased by 3.0pp from the previous quarter to 61.6%, the largest increase in share since 2024 Q3, but remained 2.0pp lower than a year earlier (Chart 5).

- The share of gross advances for remortgages for owner occupation decreased by 3.1pp from the previous quarter to 25.4%, the largest decrease since 2024 Q3, but remained 1.9pp higher than a year earlier (Chart 5).

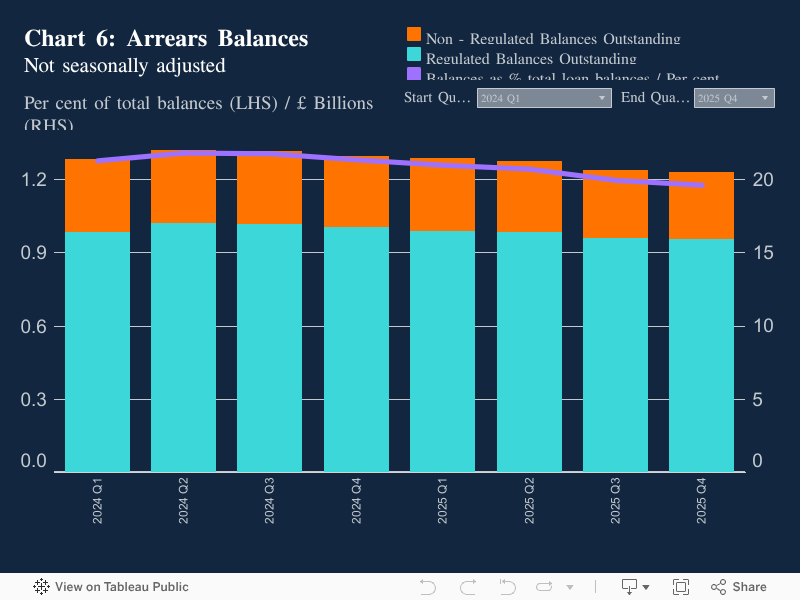

- The value of outstanding mortgage balances with arrears decreased by 0.9% from the previous quarter to £20.4 billion, the lowest since 2023 Q3, and was 5.3% lower than a year earlier (Chart 6).

- The proportion of the total mortgage loan balances with arrears, relative to all outstanding mortgage balances, has stayed the same as the previous quarter at 1.2%, and was 0.1pp lower than a year earlier (Chart 6).

- The proportion of total outstanding balances with arrears that are new arrears cases increased by 0.6pp from the previous quarter to 9.4%, the first increase since 2023 Q2. This was the same as a year earlier.

Table A: Residential loans to individuals, flows and balances

Regulated and non-regulated mortgages *

£ billions

Not seasonally adjusted

|

Q1 |

Q2 |

Q3 |

Q4 |

Q1 |

Q2 |

Q3 |

Q4 |

|

|

2024 |

2025 |

|||||||

|

Flows |

||||||||

|

Gross advances |

51.6 |

60.2 |

65.5 |

68.8 |

77.6 |

58.8 |

80.4 |

79.4 |

|

New commitments |

60.2 |

66.9 |

66.1 |

69.4 |

68.3 |

78.2 |

79.4 |

69.9 |

|

Amounts outstanding |

1,670.0 |

1,676.3 |

1,674.7 |

1,683.4 |

1,702.4 |

1,707.1 |

1,721.3 |

1,734.4 |

*This data covers regulated mortgage lending, and non-regulated mortgage lending by firms which undertake regulated mortgage lending or administration of regulated mortgages.

Graphical Analysis:

- The value of gross mortgage advances decreased by 1.3% from the previous quarter to £79.4 billion, but remained 15.4% higher than a year earlier (Table A and Chart 1).2

- The value of new mortgage commitments (lending agreed to be advanced in the coming months) decreased by 11.9% from the previous quarter to £69.9 billion, the largest decrease since 2023 Q3, but remained 0.8% higher than a year earlier (Table A and Chart 1).3